Weekly Update

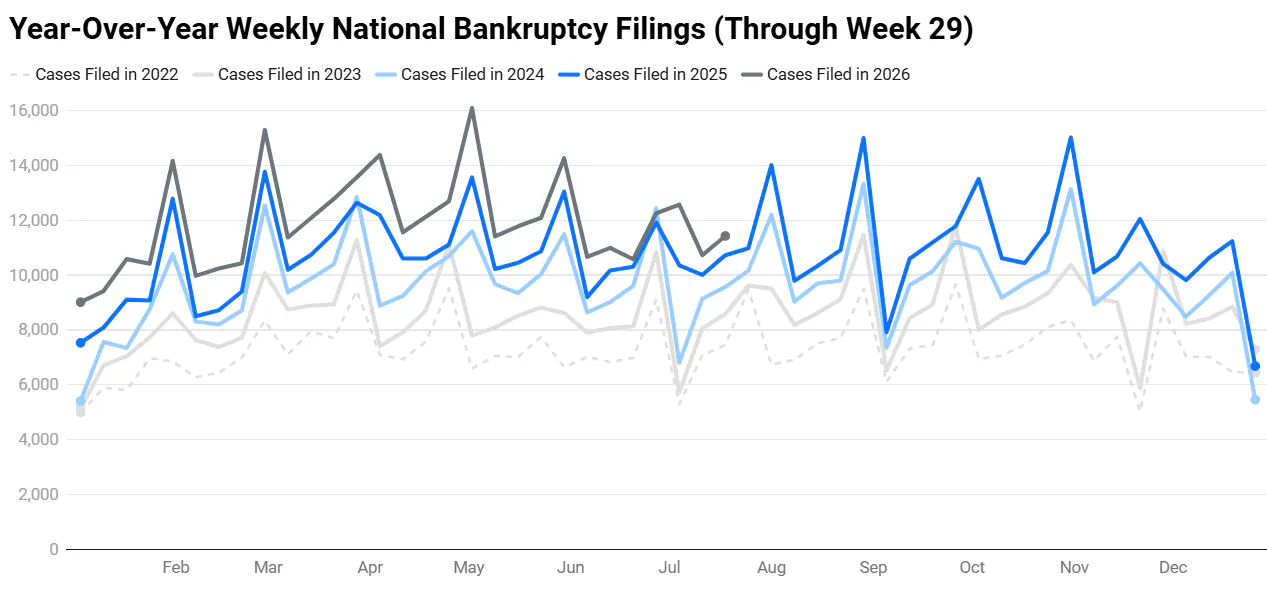

2026 Week 29 Bankruptcy Statistics: Total Filings Up 6.5% YoY

Marco Varela

July 20, 2026 · 5 min read

Real-time bankruptcy statistics to help you make better business decisions, faster. Industry market research reports, statistics, analysis, data, trends, and more.

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela

Weekly Update

Marco Varela